The Cash Conversion Cycle, also knows as Cash-to-Cash Cycle Time, is the time between when a business pays its suppliers and when the business receives payment from its customers, usually expressed in days. Keeping active tabs on your Cash Conversion Cycle will aid you in monitoring your finances as cash flows in and out of your business.

ƒ (Days Inventory Outstanding) + (Days Sales Outstanding) - (Days Payables Outstanding)

It takes a widget manufacturer an average of 60 days to sell its inventory, and then having sold their widgets, takes them an additional 30 days to collect cash. In general the manufacturer pays its suppliers in 75 days.

Cash-to-Cash Cycle Time = 60 Days Inventory Outstanding + 30 Days Sales Outstanding - 75 Days Payables Outstanding = 15 days.

Note: Calculations for the components:

DIO = Average Inventory / COGS X 365 (if values are annual)

DSO = Average Accounts Receivable / Revenue Per Day

DPO = Average Accounts Payable / COGS Per Day

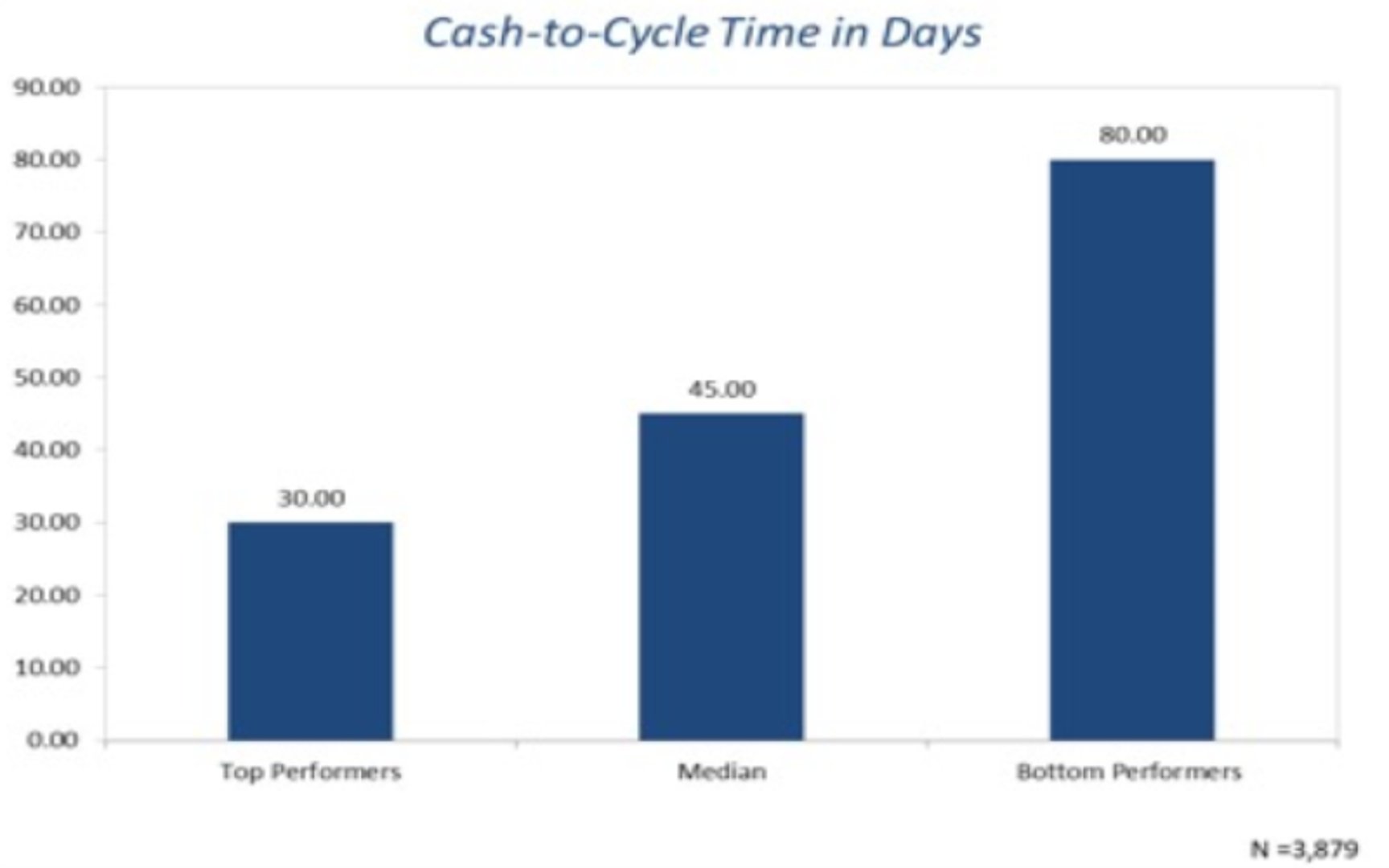

Although you should target a shorter cash-to-cash cycle time, the benchmark for this metric is between 30 to 45 days in general, according to APCQ's benchmark research.

There's two ways you can look at your Cash Conversion Cycle data: track changes (which can indicate improvements or declined performance) over time or compare two periods of time to pinpoint specific events that may have triggered change in cycle time.

Cash Conversion Cycle is financially important in your efforts to set expectations between a vendor and carrier, establishing a cadence of regular, predictable payments. In an asset-driven industry with products moving through your company quickly, keeping track of cash flows is a financial make or break for your business. This metric is also commonly referred to as Cash-to-Cash Cycle Time.

Aside from finances, cash-to-cash cycles can indicate changes in the health of your supply chain. Lower cycle times can symbolize a more profitable, lean business. Additionally, the metric can be a sign of how efficiently you’re using your assets and resources to deliver reliably.

Ideally, you should shoot for low cash-to-cash cycle times. However, your target number should result from a balanced consideration of supplier and customer needs.

A Cash Conversion Cycle that is too low may leave you with insufficient inventory or with late payments to suppliers. Your target metric should reflect your aim to meet the needs of all parties involved.

Monitoring Cash Conversion Cycle will benefit both your asset management performance and financial tracking abilities.